Payday Lenders Cry Crocodile Tears After CFPB Properly Categorizes Suspicious Public Comments Opposing Payday Rule

RHETORIC: The payday lending industry’s main trade group says the CFPB is incorrectly categorizing public comments that opposed the Bureau’s proposed payday lending rule as “duplicative, mass mail, or form letters—when they clearly are not.”

Politico reported on April 18 that payday lenders are upset with the Consumer Financial Protection Bureau (CFPB) over its “handling of comments on a rule that would require lenders to make sure their borrowers have the ability to repay their loans.”

The story goes on to quote a letter from the industry’s special interest trade group, the Community Financial Services Association of America (CFSA):

“We have grave concerns about the process by which the Bureau is reviewing and classifying submitted comments. In particular, we remain concerned that the process currently in place is serving to overlook the content of individual comment letters by classifying them as duplicative, mass mail, or form letters—when they clearly are not.

“…By misclassifying thousands of comments submitted by individuals, the Bureau is improperly marginalizing the opinions of the very consumers it is charged with protecting.”

REALITY: The same payday trade group crying foul today once attacked the CFPB for attempting to hide supposedly personal stories supporting lenders. These stories used many of the exact same sentences and paragraphs, word-for-word.

The CFSA, which is now crying foul, chastised the CFPB in a September, 2016, press release bearing the accusatory headline, “CFPB Buried, Ignored Positive Payday Loan Customer ‘Tell Your Story’ Testimonials It Requested.” What the CFSA neglected to include in its release is the startling fact that many of the supposedly personal stories submitted to the CFPB included some of the exact same sentences. For example:

- “There are no other products out there that give you the freedom that a pay day loan can give you,” appears in at least forty-three different stories.

- “It was a very efficient process and definitely the most reasonable option for me,” appears in at least eighteen different stories.

- “Medical bills can be very difficult to get under control and are very confusing. This loan was a great solution for me,” appeared in at least twenty-eight different stories.

- “After doing a little research online, I found that payday loans were exactly the option I needed. I was able to walk in and sit down with someone who explained everything easily to me and I got my money in no time,” appeared in at least fifteen different stories.

- “To avoid bouncing a check, I turned to a loan to help pay some bills. I found that it was a great choice for me and I was able to pay my power bill on time and without penalty,” appeared in at least forty-nine different stories.

- “These can really put a hurt on our wallet but after getting a short-term loan, we do not have to worry as much about the payments and can focus on staying healthy,” appeared in at least thirty different stories.

- “I’ve recommended pay day loans to people and used them myself, and everyone I’ve talked to has had a good experience and is grateful for the small loans they get. I’m not sure what many of us would do if we could not take out these loans any more. The government should leave them alone since they help so many families,” appeared in at least seventeen different stories.

- “I work long hours and do not have time to get to a regular bank or wait for my paycheck to clear so I can pay bills. I do not have confidence that the bank will work with me when I’m in a pinch for cash, but I know that a payday loan shop will. They get that I need money right away and will pay the advance back as soon as I can, without a bunch of paperwork or surprises,” appeared in at least twenty-two different stories.

The stories submitted are not identical. They do not appear to be the result of an online petition. In fact, the CFPB’s “Tell Your Story” portal does not offer any sample language. Instead, these stories are largely unique but include a suspiciously significant number of identical sentences and paragraphs. It is important to note that the Allied Progress review of these CFSA-championed stories was not comprehensive. A more thorough examination would undoubtedly result in many more examples of identical phrasing appearing in these purportedly personal story submissions. [“CFPB Buried, Ignored Positive Payday Loan Customer ‘Tell Your Story’ Testimonials It Requested,” September 6, 2016, Community Financial Services Association of America website, accessed September 13, 2016; “Tell Your Story” submissions from January 21, 2016, Consumer Financial Protection Bureau website, accessed September 13, 2016; and “Tell Your Story” submission portal, Consumer Financial Protection Bureau website, accessed September 13, 2016.]

REALITY: In just minutes Allied Progress found hundreds of public comments opposing the CFPB’s proposed payday lending rule also included many of the exact same sentences and paragraphs.

Like the “Tell Your Story” submissions praising payday loans, many of the public comments submitted in opposition to the CFPB’s proposed payday lending rule include identical sentences and paragraphs. Take the following comment, for example, from Miko Jaleel. Nothing about it is unique. Every sentence appears in other comments allegedly submitted to the CFPB by other people. [“Comment Submitted by Miko Jaleel” on the CFPB Proposed Rule: Payday, Vehicle Title, and Certain High-Cost Installment Loans (Docket No. CFPB-2016-0025), Regulations.gov website, accessed September 13, 2016.]

From: Miko Jaleel

To: CFPB_FederalRegisterComments

Subject: docket number CFPB-2016-0025

Date: Wednesday, July 13, 2016 9:14:59 PM

Even though I had insurance to help cover some of the costs of my car repair, I still needed some extra money to get a rental. Payday loans gave me the money so I could afford it and I’m glad they were able to help me.

I can afford my phone bill most of the time, but there are times that I have extra costs that do not fit my budget. To keep my budget on track, I rely on pay day loans.

Without these loans, I would not have anywhere else to go when the bills get too high. I’m afraid that this limit will leave me with no options if I’m in a bind. The new CFPB rules will only hurt me and won’t solve anything.

Shutting down payday loan stores would hurt the many families that rely on these loans in order to stay out of bankruptcy. It is important to keep this loan option as it is.

Miko Jaleel

When each of the sentences in this randomly selected comment is searched in the regulations.gov comment database for the CFPB’s proposed payday lending rule, it returns numerous examples of the exact same sentence being used in comments submitted by other individuals:

- “Even though I had insurance to help cover some of the costs of my car repair, I still needed some extra money to get a rental. Payday loans gave me the money so I could afford it and I’m glad they were able to help me,” appears in at least 101 other submitted comments. [Docket Browser search results (101) from Comments on CFPB-2016-0025, Regulations.gov website, accessed April 18, 2017.]

- “I can afford my phone bill most of the time, but there are times that I have extra costs that do not fit my budget. To keep my budget on track, I rely on pay day loans,” appears in at least 273 other submitted comments. [Docket Browser search results (273) from Comments on CFPB-2016-0025, Regulations.gov website, accessed April 18, 2017.]

- “Without these loans, I would not have anywhere else to go when the bills get too high. I’m afraid that this limit will leave me with no options if I’m in a bind,” appears in at least 115 other submitted comments. [Docket Browser search results (115) from Comments on CFPB-2016-0025, Regulations.gov website, accessed April 18, 2017.]

- “The new CFPB rules will only hurt me and won’t solve anything,” appears in at least 115 other submitted comments. [Docket Browser search results (115) from Comments on CFPB-2016-0025, Regulations.gov website, accessed April 18, 2017.]

- “Shutting down payday loan stores would hurt the many families that rely on these loans in order to stay out of bankruptcy,” appears in at least 300 other submitted comments. [Docket Browser search results (300) from Comments on CFPB-2016-0025, Regulations.gov website, accessed April 18, 2017.]

- “It is important to keep this loan option as it is,” appears in at least 578 other submitted comments. [Docket Browser search results (578) from Comments on CFPB-2016-0025, Regulations.gov website, accessed September 15, 2016.]

This exercise could be repeated time and again to turn up hundreds, if not thousands of other examples of supposedly personal and unique comments submitted directly to the CFPB in opposition to its proposed rule that include at least some of the exact same sentences found in the comments of other individuals.

REALITY: Payday Lenders Have a History of Engaging in Unethical Behavior to Influence Government Regulators

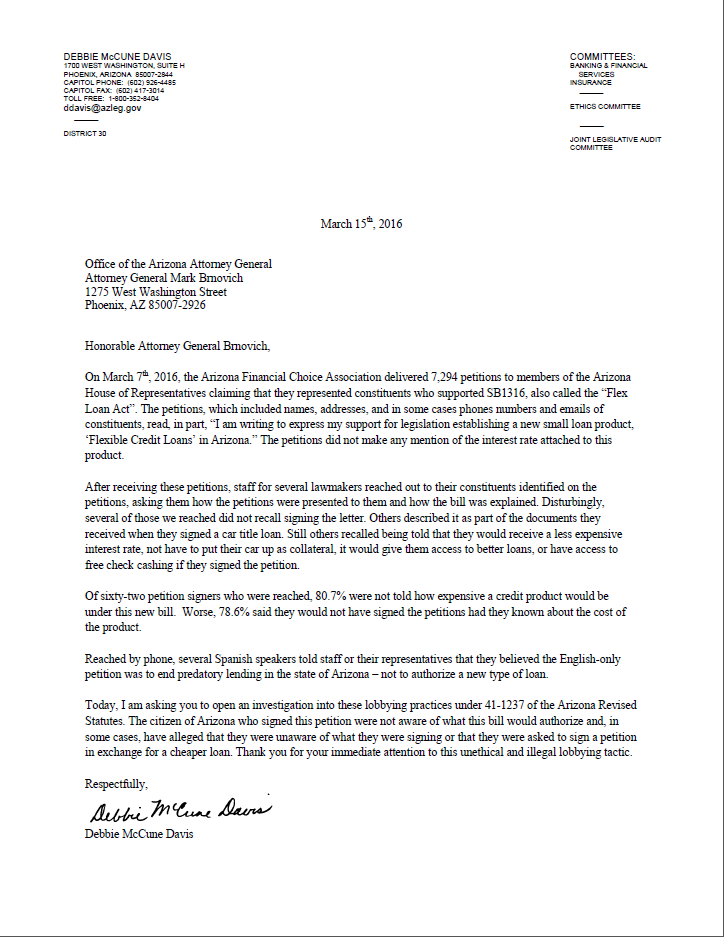

In state-based payday lending campaigns, industry groups have resorted to questionable tactics in an attempt to influence state lawmakers and achieve their regulatory goals. In January, the pro-payday group Arizona Financial Choice Association organized a purported letter-writing campaign of borrowers supporting SB 1316, legislation that would legalize predatory loans with triple digit interest rates in the state. According to State Representative Debbie McCune Davis, who requested a State Attorney General investigation into the industry-backed effort, when letter signers were contacted and told exactly what the bill would entail, many fully opposed it. Signers also admitted that they were told to sign the letters as part of their loan application. Worse still, some did not recall signing the letters at all. [“Rep. McCune Davis Asks AG to Investigate Arizona Financial Choice Association for Misrepresentation,” Arizona House Democrats (blog), March 15, 2016; and Rep. Debbie McCune Davis to Attorney General Mark Brnovich, 15 March 2016, Arizona House Democrats (blog).]

{kind=link}

For the better part of a year, while the CFPB was still preparing its payday lending rule, the industry-supportive astroturf group Protect America’s Consumers was pummeling the bureau with a barrage of inaccurate television and digital ads around the country. The only person publicly affiliated with the group, its CEO Steve Gates, once worked for an organization that was caught faking grassroots activity, even forging letters to members of Congress. That phony activism was subcontracted to Lincoln Strategy Group, which also appears to be running the anti-CFPB astroturf operation for Protect America’s Consumers. Lincoln Strategy Group is run by Nathan Sproul, who’s companies have been investigated in multiple states and by the FBI for violating voter registration laws. [Allied Progress, Reality Check: Shadowy Front Group Running Grossly Misleading Ads about CFPB Pay and Office Construction Costs, February 24, 2016, accessed September 13, 2016; Allied Progress, Latest ‘Protect America’s Consumers’ Ads Targeting Senators Riddled with Misinformation, April 11, 2016, accessed September 13, 2016; and Allied Progress, Shady Astroturf Group Creates Anti-CFPB Attack Ad about Pretend Donors to Pretend Campaign, May 4, 2016, accessed September 13, 2016; Isaac Arnsdorf, Emily Kopp, and Noah Weiland, “More Anti-CFPB Shenanigans,” Politico, January 7, 2016; “Coal Lobby’s ‘Purest Form of Grassroots’ Delivered by GOP Voter Fraud Company,” Think Progress, August 7, 2009; Isaac Arnsdorf, et al., “PI Exclusive: Uncovering the ‘Astroturf’ Firm behind the CFPB Attack Ads,” Politico, May 19, 2016; Craig Harris, “Arizona Political Operative Sproul in Spotlight,” Arizona Republic (Phoenix, AZ), October 18, 2012; Michael Walsh, “FBI Investigating Voter Registration Company Strategic Allied Consulting for Fraud,” New York Daily News, November 3, 2012; Stephanie Saul, “G.O.P. Operative Long Trailed by Allegations of Voter Fraud,” New York Times, October 5, 2012; Patrick Marley, “State GOP Linked to Dicey Firm; Party Briefly Contracted with Group under Investigation,” Milwaukee Journal Sentinel, October 14, 2012; and Eli Stokols, “Colorado Girl Registering ‘Only Romney’ Voters Tied to Firm Dumped by RNC Over Fraud,” KDVR/Fox 31 Denver, September 28, 2012.]

As The Plain Dealer reported in August 2016, there was growing concern at the time that payday loan borrowers were being pressured by lenders into submitting comments to the CFPB that oppose the proposed rule. The fact that borrowers were being asked to submit comments opposing the rule as part of the loan process, according to The Plain Dealer, suggested “that the letter-writing involves an element of coercion or pressure, directly or implied.” [Stephen Koff, “Payday Lenders Get Thousands of Borrowers to Complain to Government about Rules Meant to Protect Them,” Plain Dealer (Cleveland, OH), August 22, 2016.]

Allied Progress made these and other points in its own public comment letter on the proposed payday lending rule submitted to the CFPB in September 2016.